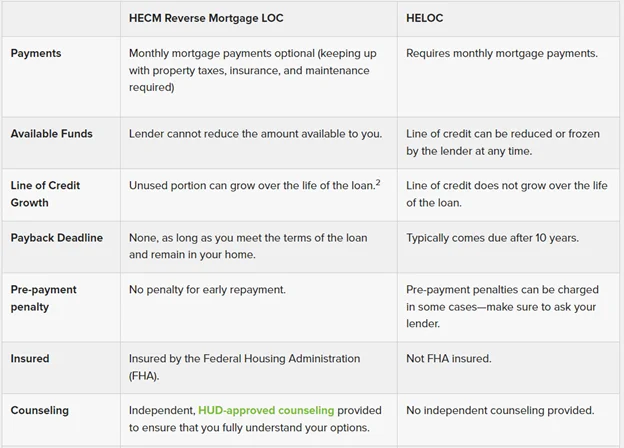

A reverse mortgage also has a line of credit feature which can provide that security.There are similarities and differences between the two options outlined below.

Before deciding between a HELOC vs. a HECM reverse mortgage line of credit, consider your short-term and long-term goals for accessing your home’s equity. If you are age 62 or older, you have several options available that other homeowners may not. Start by asking yourself the following questions:

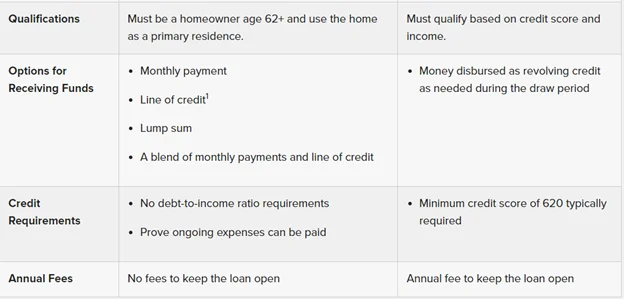

How do you plan to use the money? If you need cash for living expenses and plan to remain in your home for the foreseeable future, a HECM reverse mortgage may be your best option. A HECM loan can also work to your advantage if your goal is to reduce monthly expenses by eliminating your monthly mortgage payment. You’ll need to continue paying property taxes, insurance, and maintaining the home as you do now. If you have sufficient income but need fast cash for a one-time or short-term need, a HELOC may make sense.

Are you considering using a line of credit1 as a safety net? Many homeowners who have taken out HELOCs have quickly discovered that these types of loans are notorious for suddenly decreasing the amount available or closing the line of credit all together. This is common if the HELOC is not regularly drawn upon and used. A HECM line of credit will remain open and available even if it’s not regularly used. In fact, the HECM line of credit is commonly used by homeowners to set aside funds for unexpected expenses or emergencies because it cannot be reduced, as it is prohibited by the laws that govern HECM reverse mortgages.

How long do you plan to stay in the home? If you are planning to “age in place,” a reverse mortgage line of credit offers some compelling advantages: no required monthly mortgage payments as long as you meet the loan terms, a line of credit that can grow2, and no mandatory repayment deadline until you vacate the home. Plus, a HECM reverse mortgage is a non-recourse loan so only the property can be used as a source to repay the loan3. A HELOC does not have these guaranteed safeguards.

Do you want your heirs to inherit your home? A HECM reverse mortgage is typically repaid through the sale of the home—so if you want to pass it on to your heirs, you’ll have to plan on alternative means for the loan to be repaid4.

Are you receiving government benefits? Typically, receiving a HECM reverse mortgage credit line doesn’t affect Social Security or Medicare benefits, but may impact Medicaid or Supplemental Security Income (SSI). Talk to your financial advisor and appropriate government agencies about your specific situation.

In Summary, a Reverse Mortgage Line of Credit offers a very flexible, powerful, and beneficial option specifically designed to help retirees meet financial obligations that may arise as they age.A traditional heloc has several components that are less attractive to meet most retirees’ needs. Note that over and above the reverse mortgage line of credit option, additional options may be better solutions5.Contact me to learn about possible options specific to your circumstances.

Footnotes: