The line of credit feature is unique in that it grows over time and is guaranteed to be available to the borrower regardless of the home’s market value or the borrower’s creditworthiness. The growth rate of the line of credit is calculated and compounds based on the interest rate on the loan in addition to monthly mortgage insurance (.5%).

This means that if you don’t need all the funds at once, you can opt for a line of credit and only withdraw what you need when you need it. The remaining funds will continue to grow over time, providing you with more funds in the future. Note that interest does not accrue on the available funds on the line of credit, only on the funds you have withdrawn.

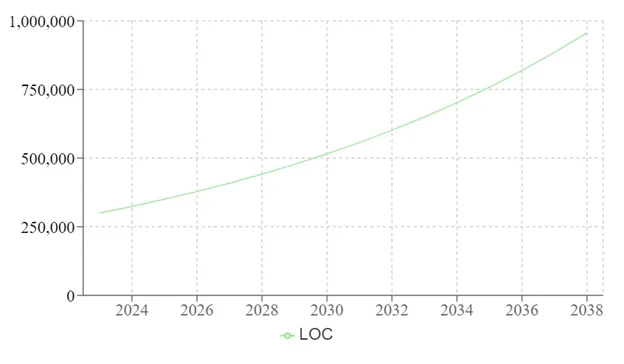

Mabel is 72 years old, has a $72,000 mortgage on her home which is worth $1,100,000. She is getting by on her monthly income but is concerned about paying for possible in-home assistance in the future. She decides to obtain a HECM reverse mortgage, pay off her current mortgage, and establish a line of credit for $300,000. Below is a graph of what the line of credit growth would be over the next 15 years. The available amount on the line of credit in 15 years would be $955,798.

If payments are made on the HECM reverse mortgage that has a line of credit, the available funds on the line of credit increase in that amount and subsequently grow (note that those payments cannot exceed the outstanding balance of the reverse mortgage).

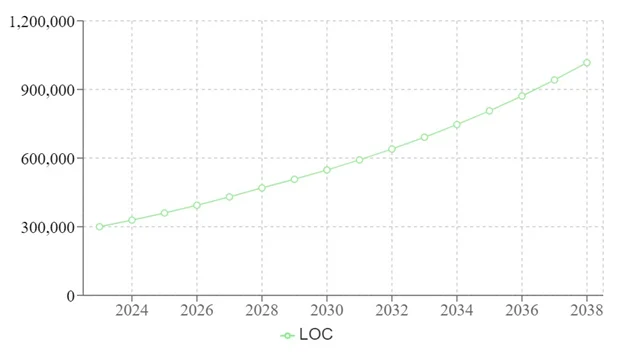

If Mabel decided to pay a nominal discretionary amount on the reverse mortgage balance of $400 per month for the first 5 years, the Line of Credit available balance would be $1,016,807 at the end of 15 years, as illustrated below.

A line of credit can be an invaluable tool for a myriad of retirees. They can use funds from the available line of credit to supply tax free cash flows in the event their portfolio experiences a down year1. A homeowner can access these funds for emergencies or unexpected expenses such as home repairs2. A retiree may elect to utilize funds from a line of credit to postpone the receipt of Social Security. Supplementing cash flow can have tax implications3 (limiting the liquidation of taxable assets) and reduce the distribution rate of an investment portfolio to provide greater longevity4.

The growth component of the line of credit feature becomes a very powerful element to a reverse mortgage.Unlike traditional lines of credit that require payments and qualifying and limit the access to funds over time depending on market conditions and property values, the reverse mortgage line of credit is available to the borrower for as long as the loan is in place5. Note that this growth feature relates to the HECM reverse mortgage line of credit.Proprietary products have a line of credit feature with different parameters6.

Understanding this component of a reverse mortgage is key to building an effective strategy to effectively manage all assets available to retirees. Contact me to find out more details about what options are available to you given your circumstances.

Footnotes: