I’ll break down both non-recurring and recurring closing costs for you:

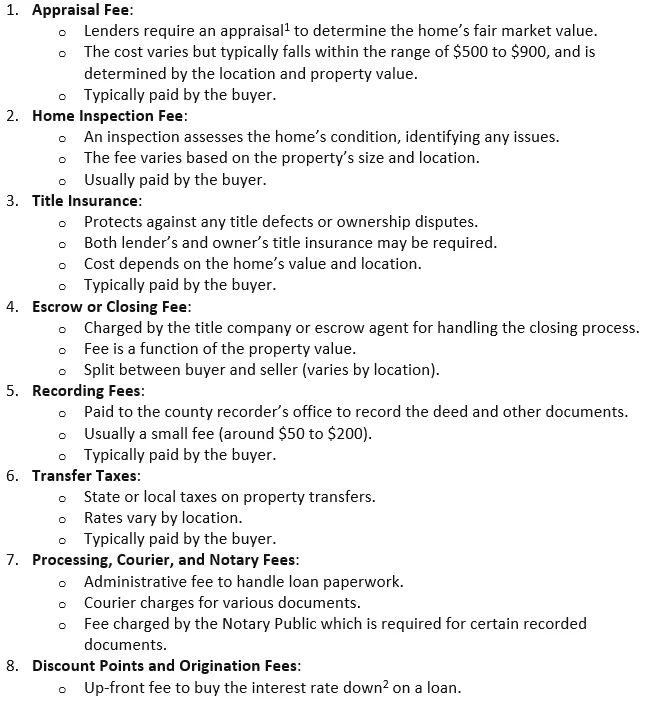

These are one-time fees that you pay during the home purchase process. They include:

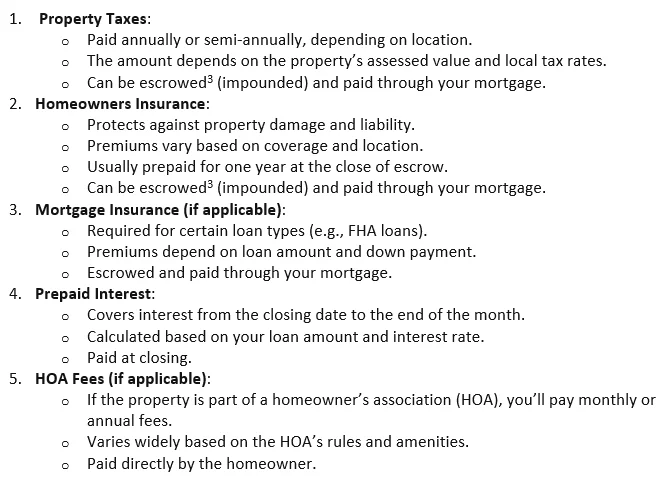

Recurring Closing Costs:

Recurring Closing Costs:These are ongoing expenses related to homeownership:

Remember that closing costs can vary based on factors like location, loan type, purchase price, and negotiations. While various locations have standard practices of who pays for each service (buyer or seller), all those particulars can be negotiated. As a buyer, it’s crucial to budget for these costs in addition to your down payment. A fee sheet can be provided to you for any particular property value for the loan program you seek.

Remember that closing costs can vary based on factors like location, loan type, purchase price, and negotiations. While various locations have standard practices of who pays for each service (buyer or seller), all those particulars can be negotiated. As a buyer, it’s crucial to budget for these costs in addition to your down payment. A fee sheet can be provided to you for any particular property value for the loan program you seek.Footnotes:

1.) See Appraisal: What is it and how is it Calculated?

2.) See Mortgage 301: Mortgage Strategies

3.) Escrow accounts or impound accounts are synonymous terms and allow a mortgage holder to pay 1/12 of their annual property tax assessment and Homeowners insurance with each monthly payment. The loan servicer accumulates those funds and pays them when due. Some programs require impound accounts, and other programs allow you the flexibility to have them or not.